YELLOW TABLE

SALES HOLDING FIRM

Sales for the world’s top construction equipment manufacturers remains resilient despite challenges

Construction equipment manufacturers have faced an unusual situation over the last few years – they’ve had to contend with issues such as rising materials and labour costs, a lack of workers, and supply chain issues, while the demand for their products has, in many cases, never been as strong.

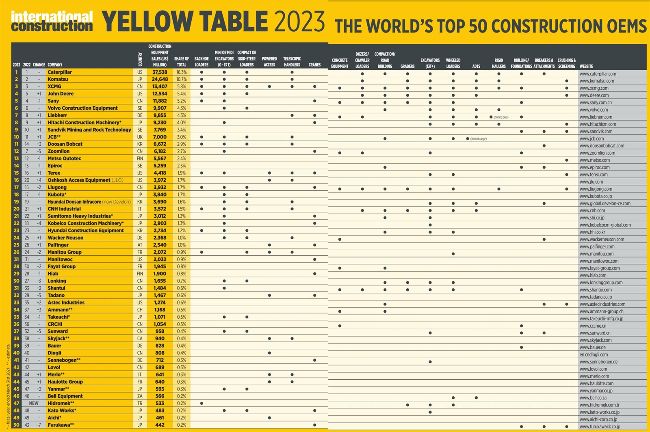

This year’s Yellow Table – which compiles the sales figures for the world’s top 50 OEMs – is looking at sales for 2022. It follows last year’s table, which saw the top 50 OEMs on the list generate the most money in the history of the Yellow Table. It is fairly impressive that in this year’s table there’s not been much change in the amount of dollars generated; the total amount is US$230.6 billion, just 0.4% less than last year’s US$232.7 billion. Regarding equipment sales, 2022 saw a couple of big changes from 2021. The first occurred in China; when equipment sales dropped in most of the world due to the impact of the pandemic, they actually rose in China in 2020 and remained high in 2021 due to stimulus spending. However, the drying up of this, aligned with the country’s zero-Covid policy hampered business and sales fell fairly sharply for most OEMs in this market in 2022.

What balanced this out is that sales improved in most other major markets. Europe saw growth as did India and North America – with this region performing very strongly, with industry experts Off-Highway Research estimating that equipment sales were up 8%. This strength is illustrated by the company – once again – taking the top spot in the list, Caterpillar.

Top ten

Sales for Cat’s construction and resources division increased from US$32 billion in the last table to US$37 billion with the gap between it and second-placed Komatsu, and the rest of the table, increasing further. Komatsu saw its sales decline slightly when adjusted for currency calculations and XCMG remained in third position, meaning that the top three are unchanged from last year.

METHODOLOGY

Positions in the Yellow Table are based on sales in the 2022 calendar year in US Dollars. Currencies have been converted to Dollars based on the average exchange rate over the course of 2022 to try and ensure fairness. Data was gathered from a variety of sources including audited accounts, company statements and reputable third-party sources. In Japan, India, and certain other countries, the use of the fiscal year (ending 31 March) has made it impossible to establish calendar year information. In these cases, fiscal year results were used. In some cases International Construction has made an estimate of revenues based on historical data and industry trends. Where this has occurred, it has been clearly marked with two asterixs’. While every effort has been made to ensure this report’s information is accurate, International Construction does not accept any liability for errors or omissions. If you would like to comment on the Yellow Table, or feel your company should be included, please e-mail the editor at: andy.brown@khl.com

SHARE OF YELLOW TABLE REVENUES

Revenues generated in the Yellow Table from firms in Asia have fallen from over half of the total amount last year (50.2%) to 44.8%. It can be argued this is a healthier figure for the industry as it means that it is not so heavily dependent on one region.

The main reason for this decline is China, which saw the revenue generated by its OEMs drop to 18.2%. North America sees an increase from 23.2% to 27.2%, helped by the strong showing of Caterpillar and John Deere, which is now the fourth largest OEM. Europe saw a marginal increase from last year’s percentage of 26.3% to 27.5%. Europe has four companies in the top ten: Volvo CE at six, Liebherr at seven, Sandvik at nine and JCB at ten.

Please note that these figures represent the revenues of the companies listed on the Yellow Table, and are therefore not representative of the revenues generated within the regions themselves or individual countries as a whole.

China-based OEMs have been increasingly focused on expanding their sales in overseas markets and this strategy enabled XCMG to hold onto third position – just – from John Deere, but Sany slip one place to fifth, overtaken by John Deere. Since the acquisition of the Wirtgen Group Deere has been steadily climbing the table over the last few years. Volvo CE is the highest European-placed company in the table, with the OEM remaining in sixth position.

Liebherr climbed to seventh place (they also increased their placing by one last year) and are followed by companies that climb one place: Hitachi Construction Machinery, Sandvik and JCB. The UK-based company returns to the top ten with the uptick in India, the largest market for JCB, helping to boost sales. These companies all rise one place in part due to China-based Zoomlion dropping from seventh position last year to number 12 on the list. This is a fairly steep drop, but it should be noted that the OEM has risen rapidly on the table in the last few years.

Movers and shakers

Some of the best performing OEMs are those that have a focus on specific products.

Oshkosh Access Equipment (JLG) is up four places, the biggest rise on this year’s table and China-based CRCHI, which specializes in tunnelling, maintains its position despite the falling Chinese market. Last year saw a fairly large change in the Yellow Table as, due to Hyundai Heavy Industries’ purchase of Doosan Infracore it became Hyundai Doosan Infracore and a subsidiary of the new Hyundai Genuine group, of which Hyundai Construction Equipment is also a subsidiary. Hyundai Doosan Infracore has since been rebranded as Develon. As Doosan Bobcat is continuing to operate as an independent business it was listed as a ‘new entry’ on the last table at number 14.

The compact specialist is performing strongly and rose to just one place outside the top ten on this table. If the sales for sister companies Develon and Hyundai Construction Equipment were combined then they would be 12th on the table. There is one new entry onto the table, Hidromek. The Turkey-based OEM has been on the list before and only narrowly did not make the top 50 last year. The OEM that just misses out this year (the 51st company) is Chinese access manufacturer, Sinoboom.

SALES REMAIN REMARKABLY STRONG

The last table was the first since the world, generally, emerged from lockdowns due to the Covid-19 pandemic and therefore it was expected that sales would rise. The sheer scale of the rise, to the highest figure ever recorded on the Yellow Table was a bit more surprising. It is therefore impressive that this year’s table sees just a 0.4% decline in sales from this record amount. It is likely that in next year’s table sales will decline again, and by more than 0.4%.

This doesn’t mean that construction will have a bad year, just that the previous years’ levels are unsustainable. OEMs are still reporting strong order books and governments around the world are continuing to invest in infrastructure projects – some on a truly huge scale. Supply chain issues and worries over spiralling inflation are genuine concerns, as is the increasingly fractured nature of geopolitical relations, but the demand for the products made by OEMs is not going anywhere.

Even a drop of several percentage points in next year’s table would still mean, when looked at from the wider historical perspective, that the sector had performed very well.

What’s next?

In all likelihood, a slight decline in next year’s Yellow Table. The construction industry has been extremely robust to ride the waves of the global pandemic, war in Ukraine, inflationary issues and a lack of skilled workers. That this year’s Yellow Table is only 0.4% down from the largest ever figure recorded on the table is an indication of how strong 2022 actually was.

Equipment sales around the world are predicted to drop by around 7% in 2023 but the total volume of machines is still expected to be above the one million units mark. At the time of writing, OEMs have released financial results for the first quarter that were broadly positive, with order books still strong.

A lot depends on China – the market is expected to see further declines in 2023 but at what level remains to be seen. The country is continuing to invest in infrastructure as are other economies around the world, which is fuelling demand for equipment. Any decline in sales for the Yellow Table will likely be ‘soft’ and come from a position of real strength. iC